Most of us are aware that money-related conflicts are one of the most commonly cited reasons for divorce.

I’d argue that the majority of us are not taught good financial habits, or how to handle money intelligently. We don’t learn these habits in school, and unless you have the privilege of learning about financial literacy from your family or community, many of us are left to sort it out on our own through trial and a lot of error—myself included.

Most people are not just not comfortable discussing their finances with other people. In sharing the first draft of this post I was told that I was brave.

And yet, talking about money feels so important. Essential, even.

“Talking about money is a gift to everyone around you”

Sarah Von Bargen, yesandyesblog.com

Like most couples, my husband and I have different thresholds for risk. Over the years we’ve also had very different salaries, assets, beliefs, spending habits, and stories around money: what it means, how we value it, how we choose to use it, etc.

From the time I left home at 17 to go to university until I turned 35, I lived with debt. More than half of my life was spent worrying about money. Retirement seemed like a distant dream.

A combination of poor choices, bad luck, ADHD, and general lack of financial savvy kept me in a holding pattern where even though I often felt “successful” in my work, I never had a grasp on my personal finances. I always felt like I was catching up on old payments, old debts, and clawing back at years of compounding interest.

I won’t even get into the ways in which having ADHD has compounded the difficulties of staying on top of important obligations.

I got fucking tired of being in debt, and tired of not feeling in control.

I wanted mastery over my personal finances, our household finances, and our business finances.

It has taken us many years to get our financial house in order, with both our personal finances and business finances. While I wish it hadn’t taken so long, I know it’s better late than never.

For the past ~3 years or so we’ve been using the approach outlined here to shift from debt-repayment mode into wealth generation. It’s been a journey to discover the system that worked for us, and I’m sharing it here in the hopes that it may help others!

There’s a lot of context and sharing in this post, but you can also scroll to the bottom to see the summary of the system we landed on.

Quick Backstory

Ben and I have both been self-employed since 2009/10. We teamed up as a Canadian corporation in 2014. We went “all in” to buy a house in late 2017, and it cleaned out every penny we had. It was only in the aftermath of house-buying that we really understood what people meant when they say “house poor,” and realized just how much work we needed to do on our personal finances.

Ben was offered full time employment in the fall of 2019 which he accepted, and I continued to grow the business on my own. Two years later in late 2021 he returned to the business, which streamlined things even further.

At each stage in this journey we made adjustments to our approach, which I’ll get into below.

How it used to (not really) work

Before diving into the current system that we’ve landed on, I think it’s worth sharing how it used to work (or not work).

Initially we both paid ourselves an equal amount from our shared business revenue, and we divided our shared expenses amongst ourselves. One of us handled the car payments and mortgage, the other handled the house insurance, car insurance, groceries, etc.

It mostly evened out. Kind of… but also, not really.

We were paying ourselves as little as possible to “optimize for taxes.” This meant we were building up a decent runway in the business (which incurs a lower corporate tax rate), but at the expense of our personal runway and savings.

Even though the business was doing well and saving money, it felt like we were living paycheck to paycheck (because we were). We disagreed about how much runway made sense to leave in the business vs put in our own personal savings. Why were we leaving so much money in our business accounts when some of our personal debts had a 19% interest rate?

We certainly weren’t paying ourselves anywhere close to what our salaries would be if we were employed full-time!

Every time we went grocery shopping, I felt stressed because groceries were “mine” to budget for, and some grocery bills were much bigger than others. If Ben added a nice cut of Salmon or a fancy protein powder to the shopping cart, I could feel my nervous system get activated, because we were eating into my already tiny personal budget (which was already eaten up by debt repayments).

Similarly, when Ben had to pay for car maintenance, house repairs, or firewood, these purchases would eat into his personal spending. It made budgeting difficult.

Any discretionary purchases became scrutinized:

“Is that a new a jacket? Can you afford that?”

The core issue was that some of our shared expenses were variable while others were fixed. While it mostly evened out, these purchases added a small psychological burden. Sure, we could keep tabs and pay each other back for these individual purchases, but that also carried a tension and transactional nature that added unnecessary strain.

Our personal spending was mixed in with shared household expenses, which made budgeting difficult, annoying, and just plain stressful.

Our personal AND business finances needed a makeover.

I’ve read OH SO MANY money books, gone to seminars, and deep-dived into endless blogs and subreddits. I tried YNAB and Mint.

I kept meticulous budget spreadsheets and tried various apps, but nothing really stuck in terms of having a true system that I could rely on consistently and made me feel like I was in control.

SURELY there had to be a better way?!

There is/was.

I spent a good 2 years deep-diving (hyperfixating..?) on all things money and finances. Shame is a hell of a motivator!

What helped us get a handle on our finances:

- A business banking strategy (implementing an adapted version of Profit First)

- A household banking strategy (merging household finances, implementing Worry Free Money)

- A personal banking strategy (Worry Free Money + 6 Jars method)

I’m going to share the evolution of our system across each of these categories.

Implementing a Business Banking Strategy

Profit First

In my quest to become a financially savvy person, I knew it was time to read the book I’d purchased a few years prior, but just couldn’t wrap my head around. After a friend mentioned it again in one of our mastermind sessions, I finally committed to reading and implementing Profit First by Mike Michalewicz.

If you are serious about getting your business finances sorted out, this book is a must-read.

I knew that if I wanted the business to start paying us higher salaries, Ben and I needed to be aligned, and I knew I really needed to be confident about this new system.

Previously Ben had been handling most of our business bookkeeping and finances, and I had been happy to let him handle it, until I realized my ignorance put me at a decision-making disadvantage.

I was no longer comfortable with my old “Marie is bad with the numbers” story. I wanted to have more say in how we handled our business finances so that we could also improve our personal finances.

It’s all connected when you’re a husband/wife business duo.

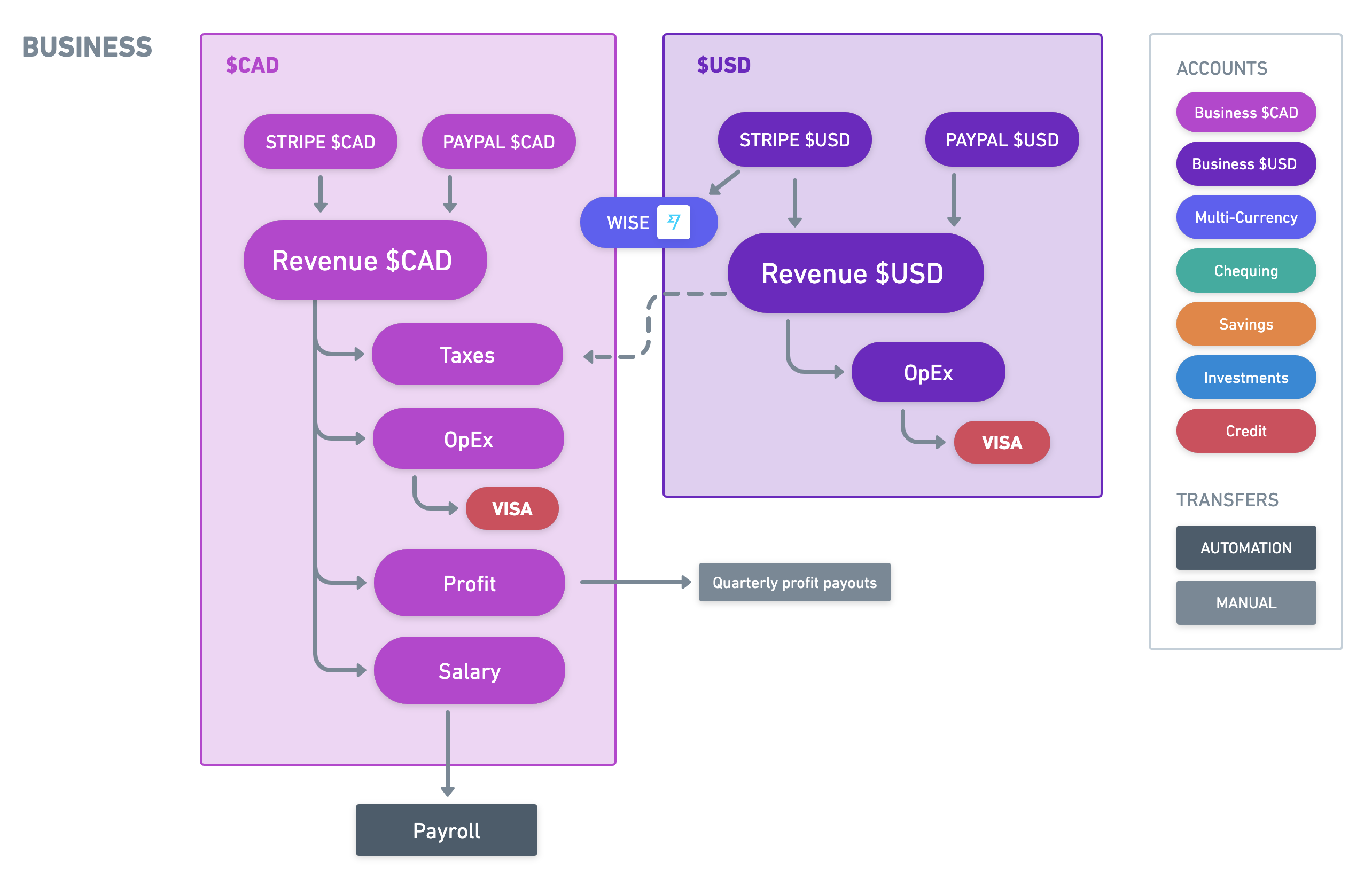

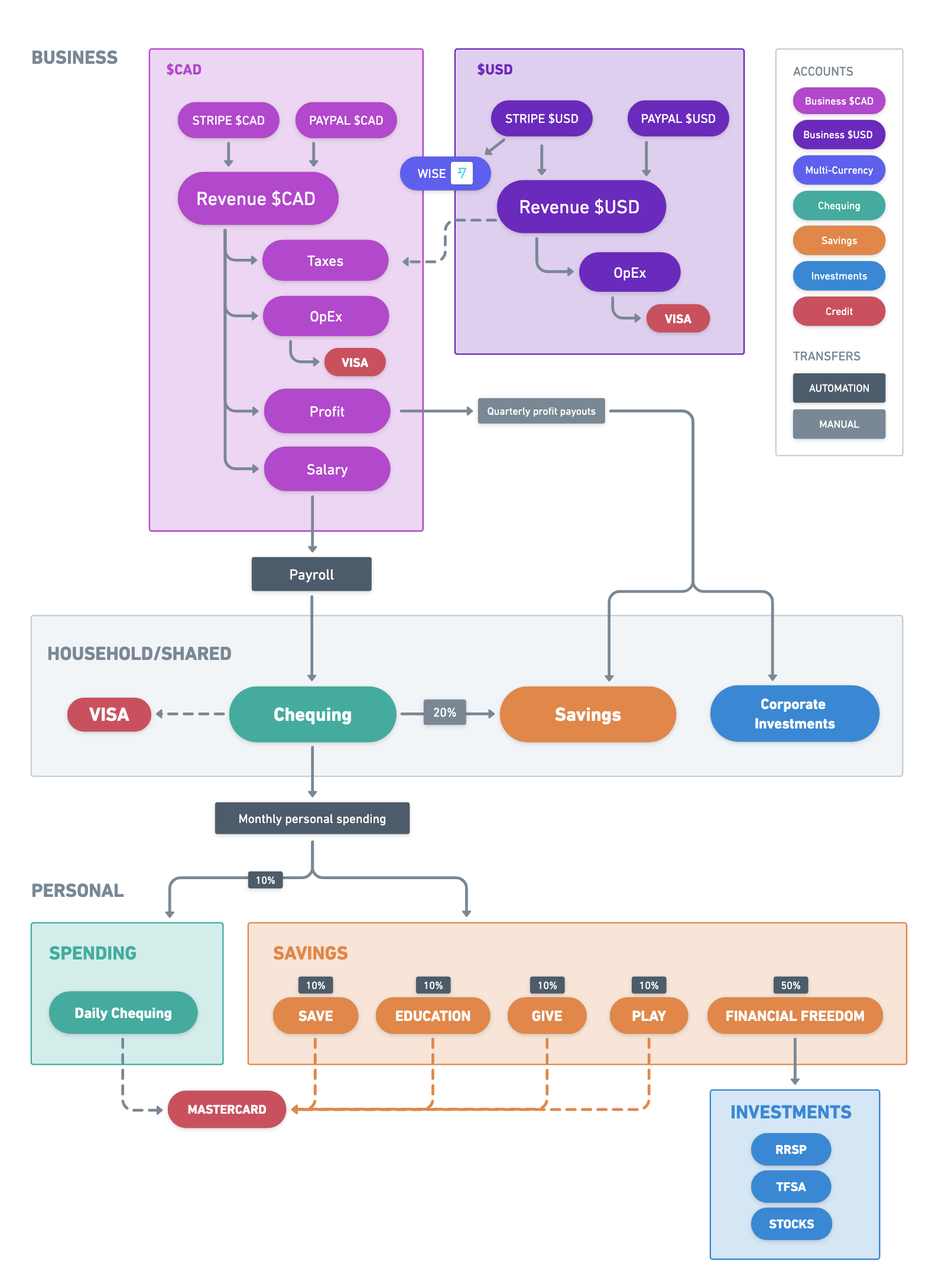

I will confess, I feel like it took me a long time to really understand the nuances of the Profit First system. Perhaps because we’re a Canadian-based company working with mostly US clients, it added a layer of complexity that required us to adapt the system for multi-currency use. This meant opening up a greater number of bank accounts than the book recommends (which already seemed like overkill!).

Did we really need that many business bank accounts?? We’re a tiny team of 2, this is madness!

Given the proportion of our USD revenue and USD expenses, accepting payment in USD and using that revenue to pay our USD expenses saves us a ton of money in currency conversion fees.

Yeah, we fought about it. Ben was skeptical about this system while I was all in, which meant I really needed to understand and believe in the system in order to get buy in from him (not dissimilar to my experience of convincing him to use *Notion, ha!)

I spoke to a variety of founders who were also doing Profit First, several of them implementing the system to varying degrees. Some were using YNAB to “allot” the money to the different categories, but they didn’t have the true separation with bank accounts that the author says is essential.

The simple concept this book is based on is this:

Previously, the traditional model of accounting looks at business profit like so:

Sales – Expenses = Profit

Michalowicz’s model flips the model around and says:

Sales – Profit = Expenses.

Now in theory, you could say that these things are the same (trust me, we argued about this at length). But we have to factor in behavioural psychology.

Mike Michalowicz’s Profit First is essentially applying Parkinson’s Law to business banking. If you take PROFIT from your account and set it aside BEFORE you allot your expenses budget, then you know that you are always profitable.

You become more discerning and frugal in your business spending. You get more creative. You notice what’s not working more quickly. You’re not waiting until the end of the year to “see how much you owe in taxes.”

BOTH Profit First (business finances) and Worry Free Money (household/personal finances) have two things in common:

- Complete separation of your bank accounts by category.

- Paying your future self first.

Profit First outlines the different bank accounts to set up:

- Profit — Savings account

- Owner’s Pay — Savings account

- Tax — Savings account

- Operating Expenses — Chequing account

- Revenue — Chequing account

I decided if we were going to do it, we needed to follow the system and make adjustments later.

It was a pain in the ass to set up all the accounts. The look on the bank teller’s face said it all. Ben’s too.

To be fair, Ben had been handling our bookkeeping up until this point, so this was definitely going to add more time to his plate, but I was WILLING to help do whatever it took to make this happen. YES, EVEN IF IT MEANT BOOKKEEPING.

Step 1: Set up all the bank accounts.

Step 2: Decide on your Target Allocation Percentages.

Step 3: Implement the twice-monthly money transfers.

Quarterly: Transfer the profits into investment accounts, and as discretionary bonuses.

We opened up a number of new accounts, and adapted it to include both Canadian and US Dollar accounts, along with a USD Visa and CAD Visa for both of us.

- Revenue CAD

- Revenue USD

- Operating Expenses CAD

- Operating Expenses USD

- Profit CAD

- Taxes CAD

- Owner’s Pay CAD

- Corporate Investment Account (WealthSimple)

- Wise (for currency conversion, and easy payout for US based contractors)

Phew.

It honestly seemed ridiculous at first (it still is), but this is where the magic happened.

Part of the reason the two of us were at odds with whether or not we had “enough” in the business bank account to pay ourselves a decent salary was that we didn’t have a true concept of how much of that money was earmarked for corporate taxes, or expenses, etc.

Looking at our business bank account, it seemed like a nice buffer to me, while Ben was worried we hadn’t put enough money away (our “runway”) for emergencies. We literally had one big business bank account that all revenue went into, and all expenses came out of (taxes, contractors, salaries, expenses, etc).

It didn’t take long of working with the Profit First system to begin seeing the benefits.

It helped us answer questions like:

- “Can we afford to send one of us to this conference?”

- “Have we set aside enough money for our corporate taxes”

- “Can we afford to bring on a new contractor?”

- “Can we afford to hire a full-time employee?”

Profit First was helping us get better visibility into the different categories of our business. It eliminated this kind of stress and uncertainty moving forward, and proved that we did in fact have the resources to increase our personal salaries.

It helped us see which expenses were essential, could be downgraded, or should be eliminated altogether. It helped us get a pulse on the health of our business, and helped us begin putting away true business profit.

After we filed our taxes, it turned out we had majorly over-saved for our payroll taxes! We had more left over in our accounts than we had paid me in salary in 2019.

That money had been sitting in our business bank account while we were—ahem—underpaying ourselves “just in case,” and struggling to pay down personal debt. This is a big part of why I was so determined to make sure I really understood our books and banking system.

The Profit First guidelines give specific numbers and percentages that made it way easier to say: yes we have the runway to increase our personal salaries.

And it took all of the emotion out of it.

Both Profit First and Worry Free Money have given us a system for better overall visibility, and a practical strategy for how to approach the day to day banking.

A catalyst

Three months into our new Profit First implementation (late summer 2019), life threw us a very interesting curveball which ultimately led us to the decision to merge our finances: Ben was offered a full-time remote role at a company based out of Toronto.

We’d both been independent/self-employed for so long, this was going to be a huge change for us in so many ways. Ben decided to take the role, which meant that our business was now essentially a company of one (yours truly).

The timing of our Profit First implementation was perfect.

Since I would be the one bringing in the entirety of our business revenue, incurring the majority of expenses, and handling day to day operations, it made sense that I should be intimately familiar with our banking strategy, cashflow, and bookkeeping methods.

I felt super confident that we were on the right track. I believe we did our first official quarterly Profit distribution and paid off all of our remaining personal debts just as Ben was starting at his new role!

Ben getting this new role opened up a ton of new conversations around our long term money goals and management.

Why?

- We were finally debt-free (other than our mortgage and a small car note), and no longer focused on “survival mode.”

- Ben was going to make a salary that was much higher than we were paying him from the business. This also meant that his personal taxes would now be coming out of his paycheck, and he would have more money available to put into RRSPs, investments, etc.

Suddenly Ben was about to have a lot more spending money AND saving money… while I was still paying myself a low personal salary.

This new imbalance in our income and the conversations that ensued brought up a lot of our insecurities and fears. It was one of the most challenging and vulnerable conversations we’d had as a couple, but we were committed to creating a mutually beneficial solution.

We were already sharing and splitting all of our household expenses, but this change was going to create a shift in spending power that would no longer feel equitable.

How the f*** do other couples manage their money together??

I spoke to anyone who was willing to talk to me about money, household finances, and investing.

I had conversations with tons of different couples of varying ages and economic situations about how they manage their money, and how they share and/or divide their household expenses and savings.

There were definitely a few different approaches; some couples had completely separate finances, while others had a shared pool regardless of their income.

Merging household finances

We outlined all of our household fixed expenses, variable expenses, as well as one-off and upcoming expenses that might impact our savings goals.

We shared our personal budgets and spending habits. We put everything on the table. We’d done this when we initially went through Worry Free Money, but it was time to do it again with a fresh lens.

We agreed that we saw one another as equals, and our goals as joint goals. We’re both ridiculously hard-working, regardless of whether we are employed or running our own business. Why should one of us get more spending (or investment) money than the other? Why should one of us feel more comfortable or secure than the other?

Ultimately, our future goals are shared. Whether it’s traveling and experiences, house renovations, or leisure activities, we’re on the same page about wanting to build a good life together.

What we did

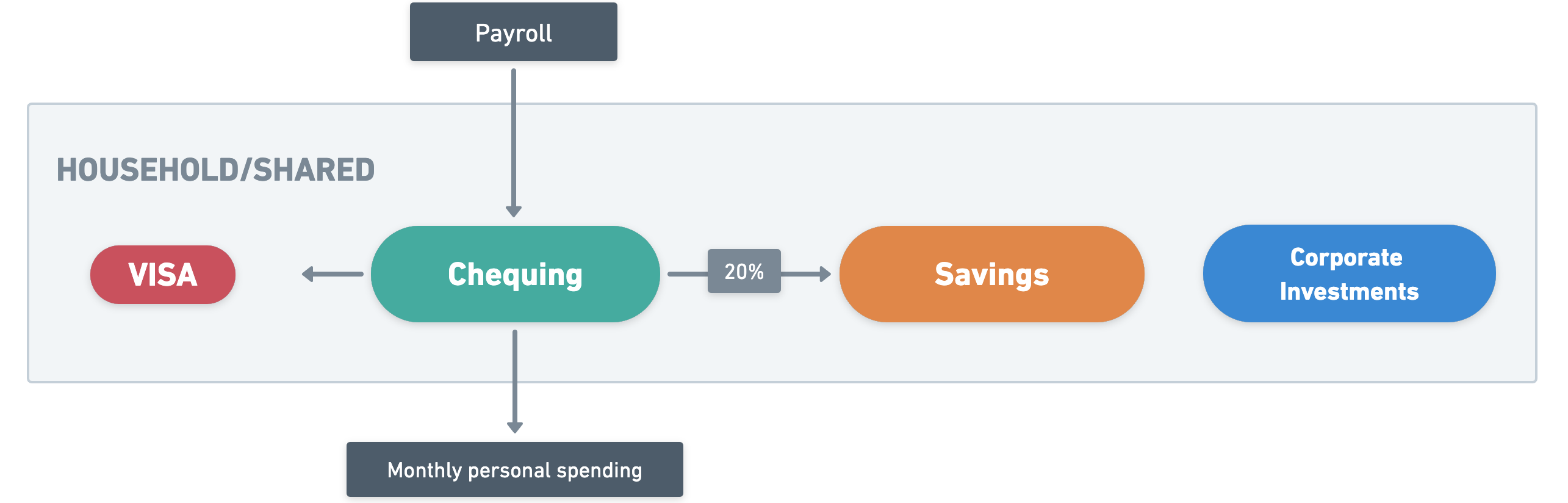

We merged our existing bank accounts.

In the end, we agreed it made sense to have a joint chequing account for all household shared spending, as well as a joint savings account.

Ben’s chequing account became our shared household expenses account, and my savings account became our joint savings account. Both of our salaries would be deposited into our joint chequing account.

We increased my salary.

We no longer needed to draw two salaries from the business, and Profit First showed us that we could afford to increase my salary, so we did.

We outlined a new household budget.

We figured out all fixed household expenses and joint savings goals. All of our fixed household necessities and expenses would be covered jointly from our shared chequing account.

We both re-read and adapted Shannon Lee Simmons’ Worry Free Money “non-budgeting” method. It’s literally the only system that has worked for my brain, AND, it was the only system that got both Ben and I on the same page about our money. I’d already been using it in my personal finances; now we were applying it together for our household finances.

We then both draw an equal amount into a personal spending account each month.

This personal amount would include an agreed-upon percentage that would go toward our respective RRSPs, TFSAs, and investments.

For any purchases that only benefit ourselves, we use our own personal spending accounts. What we each decide to do with our personal spending is truly up to each of us, no questions asked. Since we’ve had the discussion already and we already know what our savings rate is, the rest is gravy.

Worry Free Money

The Worry Free Money book is amazing and I recommend it to everyone. To summarize some of the core takeaways that we implemented:

Separating your fixed expenses from your personal spending with a completely separate bank.

It sounds so ridiculously simple and yet also… annoyingly inconvenient? But alas, this one switch changed everything. We each opened up NEW accounts at a different bank to use for our personal discretionary spending accounts.

Fewer spending categories, and no “budgeting.”

Everything is broken up into 4 categories:

- Fixed monthly costs

- Meaningful savings

- Short term savings

- and whatever is leftover is your spending money.

The idea is that once you have allotted the first 3 categories (based on your goals/needs), there’s no need to make budget categories for your spending money: you can spend this money however you wish, as long as you stay within your limit.

Since this personal spending money is in a totally separate bank account at a different bank altogether, you can “spend to zero” without guilt, and without worrying about an auto-payment you didn’t account for, or accidentally over-drafting your account.

The idea is that YES, even if you have debt, you should always have a small personal amount to work with each month. Extreme deprivation leads to “F*** it!” moments (Shannon talks about this in her book Living Debt Free: start with this one if you have debt before moving on to Worry Free Money).

The system she recommends is simple, and doesn’t require painful tracking and categorization of every purchase.

Implementing both Profit First and Worry Free Money helped us streamline things on both the business and household front.

Audit your spending.

One of the activities the book has you do is audit 3 months of spending. You look at every purchase you’ve made over the last 3 months and rate how happy those purchases made you on a scale of 1-5. Then, you want to cut out and minimize the 1-2 ratings, optimize for the 4-5 ratings, and reconsider the 3s.

We agreed that ordering Indian take-out every Thursday is a 5/5 on the happiness scale. While some people might regret their take-out purchases, for us living in a very rural area and making all our meals at home, this is a treat that we are absolutely willing to splurge on.

High quality groceries are another thing we both agreed we’re willing to budget more for. We don’t feel guilty about higher grocery bills.

On the other hand, I love getting furniture, clothing, or even plants second-hand. You get to choose where to optimize based on your goals.

The book reminds us that finances are personal, and we want to optimize for both saving for our future, while also being wise about how we spend our money now, in alignment with our values, and what makes us enjoy life.

When both partners fully understand the overall household cashflow, it’s much easier to get on the same page about spending. The key here is that these amounts are agreed upon in advance and automated, just as they are with Profit First.

EVERY TWO WEEKS:

Every 2 weeks we do our Profit First distributions and review our accounts (business and personal). We treat this like a DATE. Grab some wine or tea, put on some tunes, and snuggle up!

Together we each update a shared net worth spreadsheet which includes every single bank account, asset and liability we have together and separately. This allows us to visualize our growth in a chart which is highly motivating.

We don’t question one another’s personal savings or spending accounts. Since we’ve already agreed upon the shared household goals, the rest is up to each of us to buy in line with our values, and what we can afford.

Automate your savings, agree on the amounts in advance, and work with what’s left. Just like with Profit First, if the money isn’t available in your spending account, it’s not available for use, and it forces you to get way more creative.

We all have limited willpower—some more than others—don’t rely on willpower alone when it comes to spending. When you have a spending plan and a banking strategy, it becomes a lot easier.

After two years of working full-time, Ben returned to the business in December 2021. We continue to use the same processes and are now a team of 4 full-time employees (plus a few contractors). We’re also now able to include our employees in our profit distributions, which is an incredible feeling. While Ben getting a full-time job was a catalyst for merging our accounts, I really wish we’d done it sooner!

Personal finances

Once we had finally reached the milestone of becoming debt free, I quickly realized I needed to adapt my strategy. Previously, I had been putting 90% of my personal spending into dept repayment.

Now, for the first time in my life I had no personal debt, and no idea what to do my personal money. How much should I save? Into what kind of accounts? How do I invest? How much should I invest?

I had no idea, but just like I did before, I began talking about investing, saving, and spending with anyone who was willing. Learning about investing became my new “project.” I was ready to be smart with my money, and never wanted to get back into personal debt ever again!

What I did

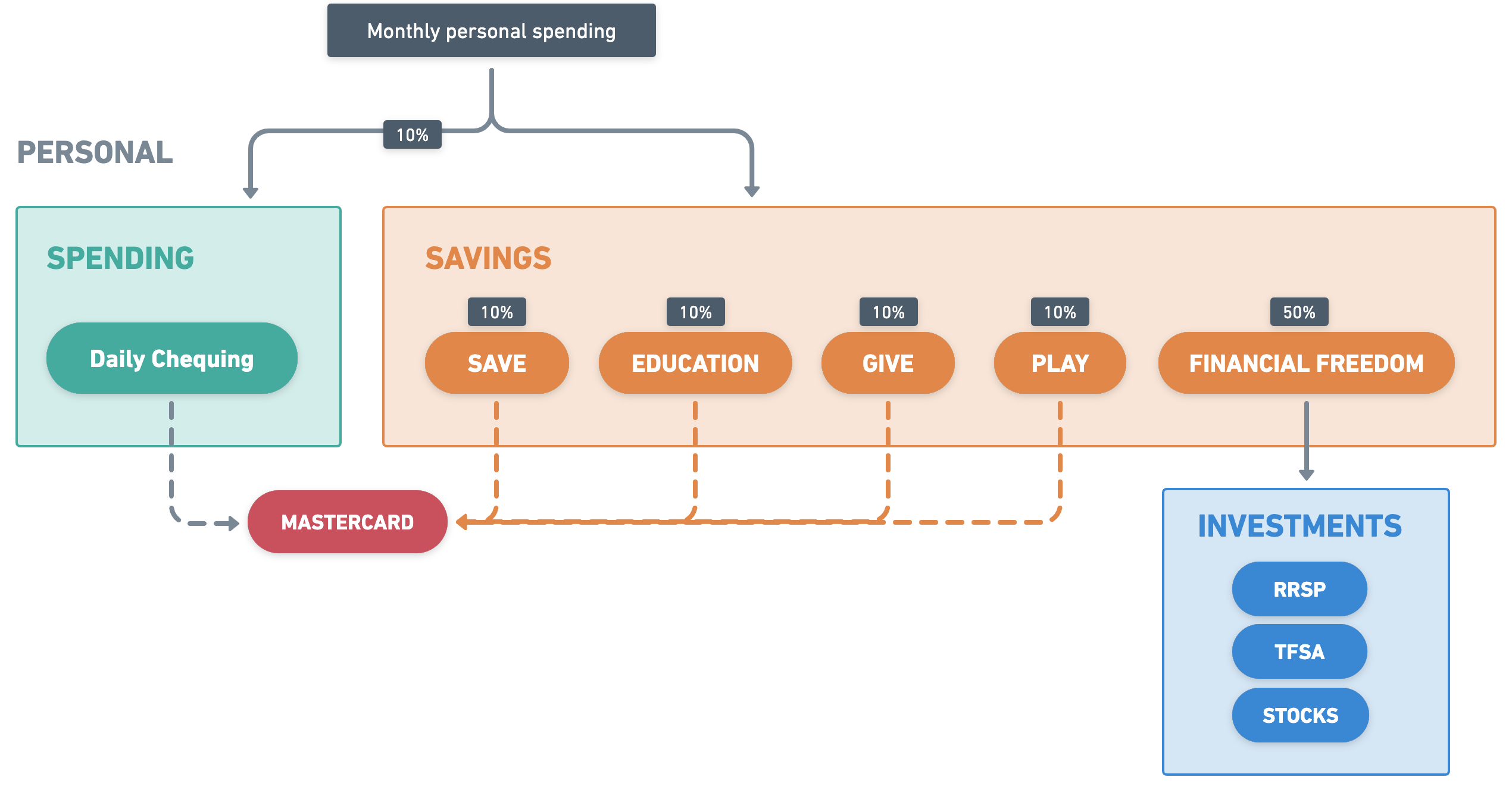

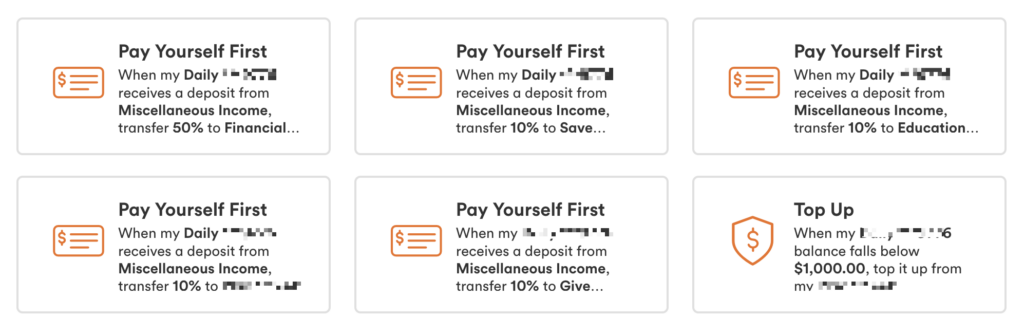

I eventually landed on a combination of the principles from Worry Free Money and T. Harv Eker’s Jars method. Each month when money is auto-transferred into my personal spending account, automated money rules send a percentage of that money into a number of account categories.

Now, if you look at the Jars method, it recommends 10% for financial freedom and 55% for necessities. But since the majority of my necessities are already handled at the shared level, technically everything that goes into this account is already “play” or spending money. I’m essentially further dividing my personal spending into the jars categories (inverting the necessities and the financial freedom category percentages).

- I opened up investment accounts with WealthSimple.

- I set up savings automations* so that any time income lands in my chequing account a percentage is transferred into 5 accounts.

- 50% is transferred into a “Financial Freedom” account. Each month automated payments are sent from this account into RRSP, TFSA, and Investment accounts (WealthSimple).

- 10% is for savings

- 10% is for education

- 10% is for play

- 10% is for giving

- 10% is left in the chequing account for spending.

- I set up investment automations: each month transfers are automated from the Financial Freedom savings account in Tangerine into different investment accounts with WealthSimple, including a TFSA, RRSP, and some trade accounts.

*Using Tangerine’s Money Rules.

Previously, that 90% savings was going straight to debt repayment! Since I’m used to that money not being available to me, I’m now sending it to investments and savings instead.

I share this because it might seem outrageous to have a “90% savings rate,” but this this is 90% of my personal spending after necessities have been dealt with.

Our shared goals are already automated, so what he does with his money is his choice!

How it looks in action

The Daily Chequing account is a “spend however you want” account. No automated bills come out of this account, so I can spend to zero if I want to. When I make a purchase from one of the savings categories (Play or Education for example), I do so from the Daily Chequing debit card or Mastercard, and then transfer the amount from the appropriate Savings account.)

The Mastercard is set to auto-pay every month from the Daily Chequing account.

Any automated personal bills (health subscriptions, hobbies, donations) use the Mastercard, and transfers are set up to automatically move money from the appropriate savings account.

For example, I have some automated monthly donations from my Mastercard. Each month, the same $ amount is transferred from the Give account to the Daily Chequing account, which is where the monthly Mastercard payment comes from.

The Save account is used for both short and long-term savings: personal trips, events, large ticket items, personal emergency savings, etc. Whenever I build up a buffer in this account, I transfer it to the Financial Freedom account. If I don’t see it, I’m unlikely to spend it!

Education is used for any kind of courses, training and learning (Permaculture Diploma and personal courses, etc)

Give is used for any kind of giving. Gifts, donations, and family emergencies (helping my sister purchase a laptop when hers died unexpectedly, or an unexpected emergency vet visit for my niece’s cat). Having this account available for these types of things has given me new motivation for being financially responsible.

Play is for anything fun! Trips to the plant shop, clothes & shoes, a spa day, etc.

Financial Freedom is a holding account from which investment transfers (to WealthSimple accounts) are automated. I never take money out of this account, it is purely for the purposes of building financial freedom through the form of investments. Any quarterly Profit First bonuses are split between this account and the Play account.

I’ve been using this system for the last few years, and have tweaked the percentages a few times as needed. This is the first time in my adult life where I feel good about my finances, and don’t feel the permeating crushing weight of money anxiety.

I’ve learned that there simply isn’t one simple system that works for everyone.

As a business owner with ADHD, I needed to find a solution that worked for my brain.

TL;DR

Our personal and business finances are a blend of both Worry Free Money (personal) and Profit First (business). The principles of both are really well aligned and have helped us design a system for managing our money as a couple that owns a business together.

At the beginning of each month:

- Ben’s salary is auto-deposited into our shared household chequing account.

- My salary is auto-deposited into our shared household chequing account.

- 20% of our combined salaries is moved into our joint savings.

- Credit card payments are paid off in full.

- We have a set amount that must remain in the chequing account to cover our mortgage, groceries, insurance, car payments, and miscellaneous household expenses, as well as a buffer. (This was all determined using the Worry Free Money system).

- An agreed upon personal spending amount is then transferred (automated) to each of our personal bank accounts (Tangerine Bank, which is super easy to open multiple new accounts at no extra charge). We both receive the same amount, and we revisit this amount quarterly when we do our quarterly Profit First payouts.

- A mutually agreed upon percentage of our personal spending money is distributed (automated) to our own personal savings and investment accounts, and the remainder is our own discretionary spending. The percentages remain regardless of how much we pay ourselves.

Part of the reason we still handle some of this saving/investing personally is that our tax optimization strategies are slightly different with Ben having American citizenship, so his RRSP and TFSA strategy is different than mine. (We worked with our accountants on this; be sure to find a professional you trust!) - Each quarter, we manually distribute profit to employees. Ben and I manually send half of our distribution into a corporate investment account, and the other half into our shared savings account. We then give ourselves a small discretionary personal bonus from our savings account.

Similar to Profit First, we put away our personal savings and investment money first, and whatever is left can be used for play. The key here is to automate as much of this as possible. Your savings rates and targets are determined based on your unique goals; this is part of the work we did with Worry Free Money.

We check in regularly, and have our finger on the pulse of our shared financial picture.

We check in every two weeks on Sundays to look at our books and report to each other about any positions we might have changed in our personal investments and how our shared investments are performing.

Finding our financial groove

It took several years of learning and trial and error, but we finally figured out a system for managing our household, business, and personal finances that actually works, and has reduced ALL tension around money.

This is a system I wish we’d implemented ages ago, and if sharing this helps even one other person, it will have been worth it.

It’s been nearly 3 years of Profit First and Worry Free Money, and we’ve finally shifted from feeling embarrassed to feeling really proud of ourselves and how far we’ve come.

Money stuff carries a shit-ton of shame. It can feel all-consuming, especially if you carry any debt, or have different habits than your partner.

While change can be painful, it was not nearly as painful as the pain of staying where I was, financially and mentally.

Committing to doing the work together as a partnership was the only way forward.

It took a lot of experimenting, reading, and adapting the processes to our unique needs.

We’ve both learned a ton in this process, and will continue to do so as our needs and goals change.

Was this helpful?

Have you found something that works for you?

Have more questions or want more specifics about how an aspect of the system works?

Hit me up on BlueSky and say hello!

[*For full disclosure, I’m a Notion Partner, so when you sign up with my link, you also help support me and my content!]

Thank you for this thorough and candid look into your financial approach! Do you use a credit card for your personal expenses? If so, how do you track which jar they’re associated with? Is it a shared card with Ben?

This has been tremendously helpful. I landed here totally randomly and am glad I did. Be sure that this article and the time and effort you put into it has helped at least that one person you hoped for : ME. Thank you so much.

Ridiculously helpful material. Thanks a lot for the effort of putting this together. Cheers!

So glad you found it helpful!!